W-2 and 1099 Income: How to File Taxes When You Have Both (2025 Guide)

Millions of Americans have both W-2 and 1099 income. Here's exactly how taxes work, what self-employment tax applies to, and how to avoid overpaying.

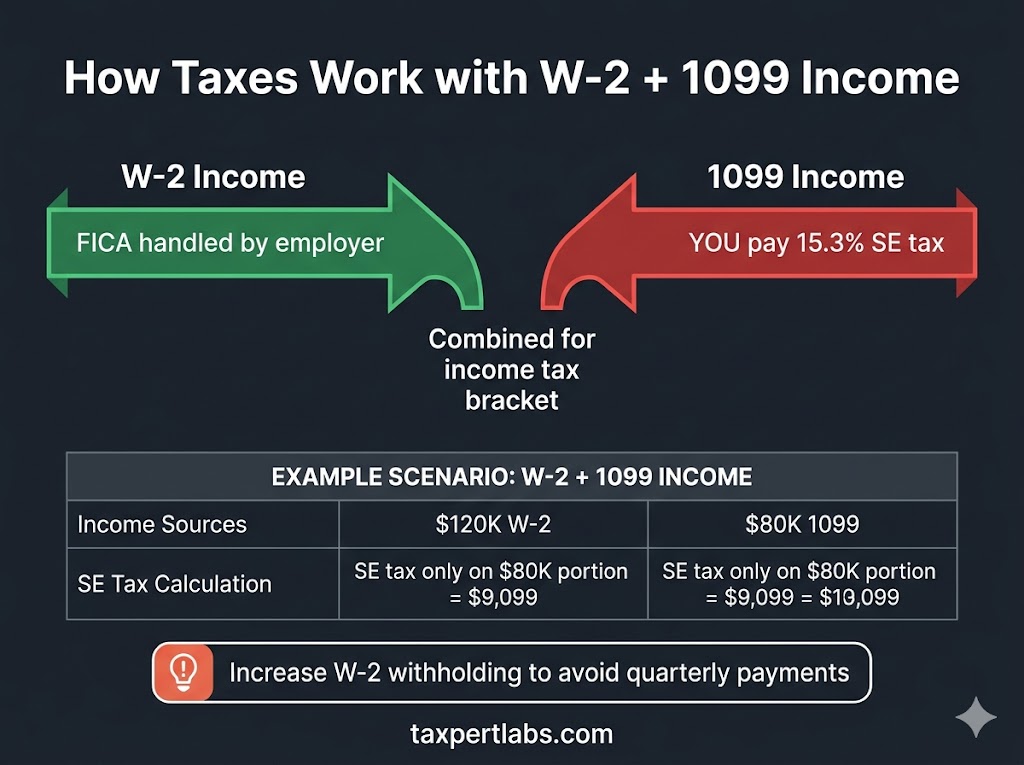

If you earn both W-2 wages from an employer and 1099 income from freelancing, consulting, or a side business, you have what the IRS calls "mixed income." Approximately 36% of the US workforce now has some form of self-employment income alongside traditional employment. The critical thing to understand: self-employment tax (15.3%) only applies to the 1099 portion of your income — not your W-2 wages. But both sources combine for income tax bracket purposes, which can push you into a higher bracket.

How does self-employment tax work with mixed W-2 and 1099 income?

Self-employment tax at 15.3% applies only to your net 1099/Schedule C income. Your W-2 employer already withholds and matches FICA (7.65% each) on your wages. The two income streams are taxed differently for payroll purposes but identically for income tax purposes. One important interaction: your W-2 wages count toward the Social Security wage base ($176,100 for 2025). If your W-2 wages exceed the cap, your 1099 income owes only the 2.9% Medicare portion of SE tax — not the full 15.3%.

Example: $120,000 W-2 + $80,000 1099

| Component | Amount |

|---|---|

| W-2 wages (FICA handled by employer) | $120,000 |

| 1099 net income | $80,000 |

| SE tax base ($80K x 92.35%) | $73,880 |

| Remaining SS wage base ($176,100 - $120,000) | $56,100 |

| SS tax on 1099 (12.4% on $56,100) | $6,956 |

| Medicare tax on 1099 (2.9% on $73,880) | $2,143 |

| Total SE tax on 1099 income | $9,099 |

How to handle quarterly estimated payments with mixed income

The simplest approach for mixed-income earners: increase your W-2 withholding by filing a new W-4 with your employer. Add enough extra withholding to cover the SE tax and income tax on your 1099 income. This eliminates the need for quarterly estimated payments entirely. Alternatively, make quarterly payments using IRS Direct Pay (irs.gov/payments) by the standard deadlines: April 15, June 16, September 15, and January 15.

When should you form an LLC for your 1099 side income?

If your 1099 net income exceeds $50,000 consistently, an LLC taxed as an S-Corp can save $5,000-$15,000+ per year in self-employment tax on that portion. The 1099 income flows through the S-Corp as salary (subject to FICA) and distributions (FICA-free). Your W-2 job is unaffected. Use our S-Corp Savings Calculator to model the math with your specific numbers.

Want to see every strategy that applies to your mixed-income situation? Run your free tax assessment — it takes 2 minutes and shows you exactly how much you could save.

Related Reading

See How Much You're Overpaying

Run a free 2-minute assessment and get your personalized tax leak report — with IRS-backed strategies and IRC code citations.

Run My Free Assessment