Self-Employment Tax: The Complete Guide to Saving $10,000-$30,000/Year (2025-2026)

The self-employment tax rate is 15.3% and it hits every dollar you earn. Here's the exact math, who pays it, and 6 IRS-backed strategies to cut it by 40-60%.

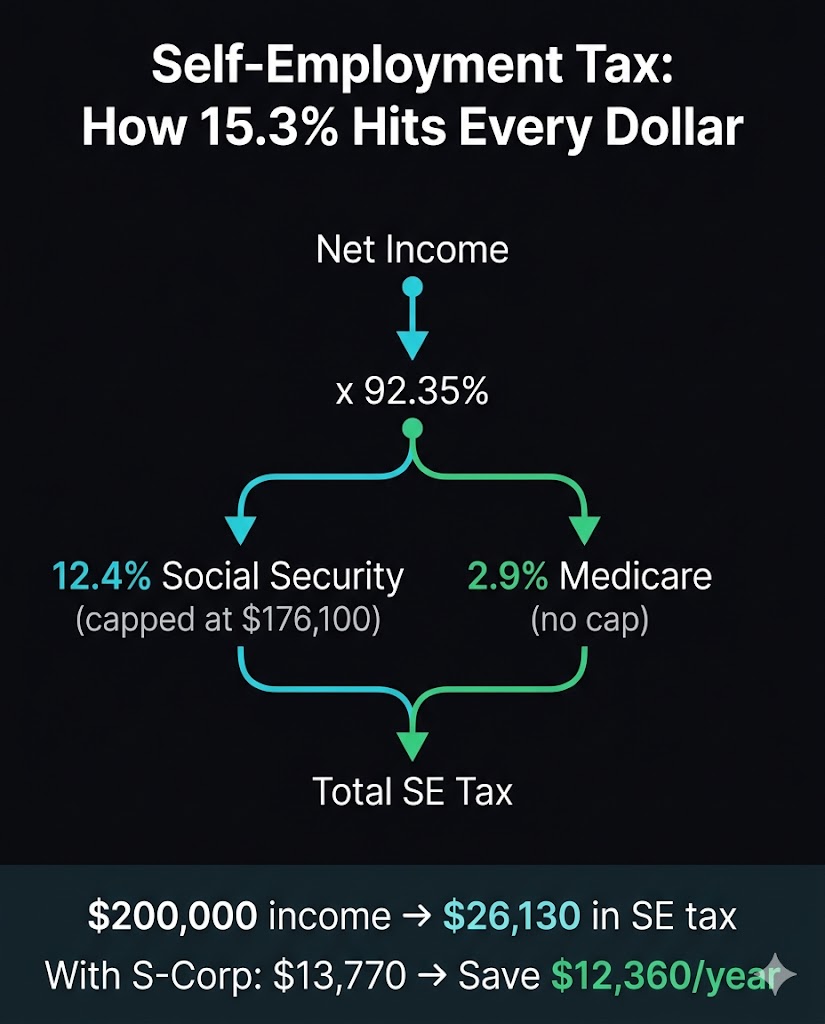

Self-employment tax is a 15.3% federal tax that applies to every dollar of net self-employment income. It funds Social Security (12.4%) and Medicare (2.9%), and it is the single largest tax most self-employed people pay — often larger than their federal income tax. On $200,000 of net income, self-employment tax alone is approximately $26,000, paid in addition to federal income tax of $35,000+. The total: over $60,000 to the IRS before you keep a dollar.

This guide covers exactly how self-employment tax works, who pays it, how to calculate it at every income level, and the 6 IRS-backed strategies that can cut your SE tax by 40-60% — saving $10,000 to $30,000+ per year.

What is the self-employment tax rate for 2025?

The self-employment tax rate for 2025 is 15.3% on net earnings up to the Social Security wage base of $176,100. This comprises 12.4% for Social Security and 2.9% for Medicare. Net earnings above $176,100 are taxed at 2.9% (Medicare only — Social Security caps out). An additional 0.9% Medicare surcharge applies to net earnings exceeding $200,000 for single filers ($250,000 married filing jointly) under IRC section 1401(b)(2).

| Component | Rate | Applies To |

|---|---|---|

| Social Security | 12.4% | First $176,100 of net SE income |

| Medicare | 2.9% | All net SE income (no cap) |

| Additional Medicare | 0.9% | Net SE income over $200K single / $250K MFJ |

| Total | 15.3% + 0.9% |

For W-2 employees, this same 15.3% is split between employee and employer (7.65% each). Self-employed individuals pay both halves. The 50% deduction (see below) partially offsets this, but the net cost is still significantly higher than W-2 employment.

How is self-employment tax calculated step by step?

Self-employment tax is calculated by multiplying net self-employment income by 92.35% (the employer-equivalent adjustment under IRC section 1402(a)(12)), then applying the Social Security and Medicare rates. The 92.35% adjustment exists because employers deduct their half of FICA as a business expense — this replicates that benefit for self-employed individuals. Here is the math at three income levels:

Example 1: $150,000 net SE income

| Step | Calculation | Amount |

|---|---|---|

| Adjusted SE income | $150,000 x 92.35% | $138,525 |

| Social Security tax | $138,525 x 12.4% | $17,177 |

| Medicare tax | $138,525 x 2.9% | $4,017 |

| Additional Medicare | $0 (under $200K) | $0 |

| Total SE tax | $21,194 | |

| 50% deduction | $10,597 |

Example 2: $250,000 net SE income

| Step | Calculation | Amount |

|---|---|---|

| Adjusted SE income | $250,000 x 92.35% | $230,875 |

| Social Security tax | $176,100 x 12.4% (capped) | $21,836 |

| Medicare tax | $230,875 x 2.9% | $6,695 |

| Additional Medicare | ($230,875 - $200,000) x 0.9% | $278 |

| Total SE tax | $28,809 | |

| 50% deduction | $14,405 |

Example 3: $400,000 net SE income

| Step | Calculation | Amount |

|---|---|---|

| Adjusted SE income | $400,000 x 92.35% | $369,400 |

| Social Security tax | $176,100 x 12.4% (capped) | $21,836 |

| Medicare tax | $369,400 x 2.9% | $10,713 |

| Additional Medicare | ($369,400 - $200,000) x 0.9% | $1,525 |

| Total SE tax | $34,074 | |

| 50% deduction | $17,037 |

Who has to pay self-employment tax?

Anyone with net self-employment earnings of $400 or more per year must pay self-employment tax. This includes 1099 independent contractors, freelancers, gig economy workers (Uber, DoorDash, Instacart, TaskRabbit), sole proprietors, general partners in a partnership, and single-member LLC owners who have not elected S-Corp taxation. If you receive a Form 1099-NEC or report income on Schedule C, you owe self-employment tax.

Who does NOT pay SE tax:

- W-2 employees (employer pays half of FICA)

- S-Corp shareholders on their distribution income (only salary is subject to FICA)

- Limited partners on their distributive share (IRC section 1402(a)(13))

- Rental income from real estate (generally exempt under IRC section 1402(a)(1))

- Investment income (dividends, interest, capital gains)

How to reduce self-employment tax: 6 IRS-backed strategies

Self-employment tax cannot be eliminated entirely if you have self-employment income, but it can be reduced by 40-60% using legitimate IRS strategies. The most effective approach combines entity restructuring with retirement contributions and deduction maximization. Each strategy below is backed by a specific Internal Revenue Code section.

Strategy 1: S-Corp election — save $10,000-$25,000/year (IRC section 1361-1379)

The S-Corp election is the single most effective way to reduce self-employment tax for business owners earning over $50,000. When you elect S-Corp taxation, your income is split into two categories: a reasonable W-2 salary (subject to FICA at 15.3%) and shareholder distributions (not subject to FICA). The savings come from the distribution portion, which completely avoids the 15.3% SE tax.

| Net Income | SE Tax (Sole Prop) | FICA (S-Corp) | Annual Savings |

|---|---|---|---|

| $100,000 | $14,130 | $7,650 (on $50K salary) | $6,480 |

| $150,000 | $21,194 | $10,710 (on $70K salary) | $10,484 |

| $250,000 | $28,809 | $15,300 (on $100K salary) | $13,509 |

| $400,000 | $34,074 | $18,360 (on $120K salary) | $15,714 |

To elect S-Corp status, file IRS Form 2553 by March 15 for the current tax year. You must set up payroll and pay yourself a reasonable salary — the IRS scrutinizes artificially low salaries. Use our free S-Corp Savings Calculator to see your exact numbers.

Strategy 2: Solo 401(k) — shelter up to $69,000 from taxes (IRC section 401(k))

A Solo 401(k) allows self-employed individuals to contribute up to $69,000 per year ($76,500 if age 50+) in tax-deductible retirement contributions. While this does not directly reduce self-employment tax (SE tax is calculated before retirement deductions), it dramatically reduces your federal income tax and AGI, which can lower exposure to the Additional Medicare Tax and other phase-outs.

With an S-Corp paying $120,000 salary: employee deferral of $23,000 plus employer contribution of $30,000 (25% of salary) = $53,000 sheltered. At a 32% marginal rate, that saves $16,960 in income tax.

Strategy 3: Maximize business deductions (IRC section 162)

Every legitimate business deduction reduces your net self-employment income, which directly reduces both SE tax and income tax. The most commonly missed deductions for self-employed professionals include home office (IRC section 280A), vehicle mileage ($0.70/mile for 2025), health insurance premiums (IRC section 162(l)), professional development, software subscriptions, and business meals (50% deductible under IRC section 274(k)). A thorough expense audit typically finds $15,000-$40,000 in missed deductions.

Strategy 4: HSA — the triple tax advantage (IRC section 223)

The Health Savings Account is the only account in the tax code with three simultaneous tax benefits: tax-deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses. Self-only contribution limit for 2025: $4,300. Family: $8,750. Requires enrollment in a High-Deductible Health Plan. While HSA contributions do not reduce SE tax directly, they reduce AGI, which lowers income tax and can reduce Additional Medicare Tax exposure.

Strategy 5: Hire family members to shift income (IRC section 3121(b)(3)(A))

If you operate as a sole proprietorship, children under 18 employed by the business are exempt from FICA tax entirely. You can pay each child up to $14,600 per year (the standard deduction) with zero tax to the child and a full business deduction for you. At a combined 35% rate (income + SE tax), that saves approximately $5,110 per child per year. The child must perform real work at a reasonable wage, and you must keep time records and job descriptions.

Strategy 6: The 50% self-employment tax deduction most people miss (IRC section 164(f))

The IRS allows you to deduct 50% of your self-employment tax as an above-the-line deduction on your personal tax return. This is not an itemized deduction — it reduces your AGI directly, which lowers your income tax bracket. On $200,000 of SE income with $26,000 in SE tax, the deduction is $13,000. At a 32% bracket, that saves $4,160 in income tax. Many self-employed individuals and even some tax preparers overlook this deduction.

Self-employment tax vs income tax: what is the difference?

Self-employment tax and federal income tax are two separate taxes. Self-employment tax (15.3%) funds Social Security and Medicare. Income tax (10-37%) funds general government operations. Both apply to self-employment income, and both must be paid. The combined effective rate for a self-employed person can exceed 40%.

| Self-Employment Tax | Federal Income Tax | |

|---|---|---|

| Rate | 15.3% (+ 0.9% over $200K) | 10-37% (progressive brackets) |

| What it funds | Social Security + Medicare | General government |

| Calculated on | 92.35% of net SE income | Taxable income after deductions |

| Deductible? | 50% deductible above-the-line | No |

| Applies to W-2? | No (employer pays half) | Yes |

| Can S-Corp reduce? | Yes — distributions exempt | Indirectly (via deductions) |

Quarterly estimated payments: avoid the underpayment penalty

Self-employed individuals must make quarterly estimated tax payments if they expect to owe $1,000 or more in taxes. Quarterly payments cover both self-employment tax and income tax. Due dates for 2026: April 15, June 16, September 15, and January 15, 2027. The safe harbor: pay 110% of last year's tax liability (for AGI over $150,000) across four equal payments to avoid all underpayment penalties, regardless of what you actually owe.

For a detailed guide on quarterly payments, see our Quarterly Estimated Taxes Guide.

Self-employment tax for specific professions

Freelancers and 1099 contractors: All 1099-NEC income is subject to SE tax. Common deductions: home office, mileage, software, phone, professional development. S-Corp election is the primary savings lever above $50K. See our 1099 Tax Strategies Guide.

Real estate agents: Commission income on 1099 is subject to SE tax. Agents have high deductible expenses (vehicle, marketing, MLS fees, licensing). S-Corp election saves $10,000-$20,000+ for top producers. See our Real Estate Tax Strategies Guide.

Gig workers (Uber, DoorDash, Instacart): All platform income minus expenses is subject to SE tax. Track every mile (business mileage is often the largest deduction). At lower income levels ($30K-$60K), the S-Corp election may not be worth the payroll cost — focus on deduction maximization.

Consultants earning $150K+: At this income level, the S-Corp election saves $12,000-$20,000/year in SE tax. Combine with a Solo 401(k) ($53,000-$69,000 sheltered) and business deductions for maximum impact. See our LLC vs S-Corp Comparison.

The bottom line: your SE tax action plan

- Calculate your SE tax using the formulas above or our S-Corp Savings Calculator

- If earning over $50K: Elect S-Corp status (Form 2553) and set up payroll

- Open a Solo 401(k) and contribute the maximum your income allows

- Audit every business expense — most self-employed people miss $15,000-$40,000 in deductions

- Set up quarterly estimated payments using the 110% safe harbor

- Get your full strategy: Run your free tax assessment to see all 35+ strategies ranked for your specific income

Every month you delay implementing these strategies costs you an estimated $800-$2,500 in taxes you do not owe. The IRS rules are clear, the math is straightforward, and the savings are immediate.

Related Reading

See How Much You're Overpaying

Run a free 2-minute assessment and get your personalized tax leak report — with IRS-backed strategies and IRC code citations.

Run My Free Assessment