How to Pay Less Tax on Rental Income in Florida: 7 IRS Strategies for Real Estate Investors

Florida rental property owners can legally reduce their tax on rental income to near-zero using depreciation, cost segregation, and the STR loophole. Here's how.

Florida real estate investors have a unique advantage: no state income tax on rental income, combined with federal strategies that can reduce the effective tax rate on rental cash flow to near zero. The tax code heavily favors real estate investors through depreciation, which creates paper losses on properties that are generating positive cash flow. This means you can collect rent, build equity, and pay little to no federal tax on the income.

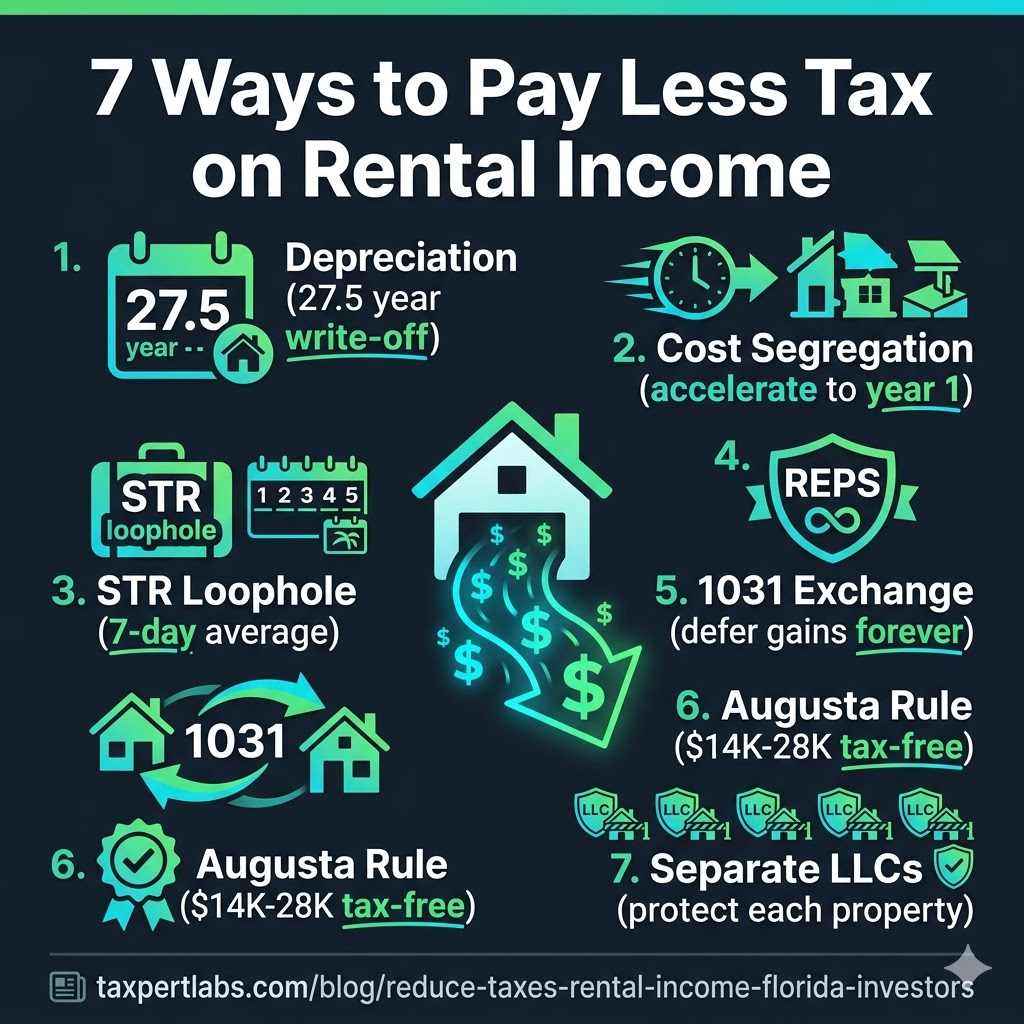

Strategy 1: Depreciation — The Foundation (IRC §167, §168)

Residential rental property depreciates over 27.5 years. On a $400,000 property (75% building, 25% land), that is $10,909 per year in deductions — money you never actually spent. Combined with mortgage interest, property taxes, insurance, and repairs, most rental properties show a paper loss even when cash flow is positive.

Strategy 2: Cost Segregation — Accelerate Everything (IRC §168(k))

A cost segregation study reclassifies building components into shorter depreciation lives:

| Component | Normal Life | After Cost Seg | Eligible for Bonus? |

|---|---|---|---|

| Building structure | 27.5 years | 27.5 years | No |

| Carpet, appliances, fixtures | 27.5 years | 5 years | Yes |

| Furniture, cabinets | 27.5 years | 7 years | Yes |

| Landscaping, parking, fencing | 27.5 years | 15 years | Yes |

On a $750,000 property, cost segregation typically reclassifies 25-35% of the building cost to shorter lives. With bonus depreciation, that can mean $60,000-$100,000+ in first-year deductions.

Strategy 3: Short-Term Rental Loophole (Treas. Reg. §1.469-1T(e)(3)(ii))

This is the strategy that lets W-2 earners and business owners use rental losses against their active income without qualifying as a Real Estate Professional:

- Average rental period of 7 days or fewer (Airbnb, VRBO)

- Material participation: 500+ hours per year managing the property

- Losses are non-passive — offset W-2, 1099, or business income directly

Combined with cost segregation, a $500,000 Airbnb can generate $80,000+ in year-one deductions against your active income.

Strategy 4: Real Estate Professional Status (IRC §469(c)(7))

If you or your spouse qualifies as a Real Estate Professional, ALL rental losses become deductible against any income:

- 750+ hours in real estate activities per year

- More than 50% of personal service hours in real estate

- Must materially participate in each rental activity (or elect to aggregate)

Strategy 5: 1031 Exchange — Defer Gains Indefinitely (IRC §1031)

Sell one investment property, buy another of equal or greater value, and defer all capital gains taxes. Do this throughout your lifetime, and at death, heirs receive a stepped-up basis under IRC §1014 — permanently eliminating all deferred gains.

Strategy 6: Augusta Rule for Property Owners (IRC §280A(g))

If you own your home and have a business, rent your home to your business for up to 14 days per year. The rental income is completely tax-free and the business gets a deduction. At $1,000-$2,000/day for a nice South Florida home, that is $14,000-$28,000 in tax-free income.

Strategy 7: Separate Entity Structure

Hold each rental property in a separate LLC for liability protection. Keep rental properties out of your S-Corp — real estate in an S-Corp loses favorable long-term capital gains treatment on sale and complicates 1031 exchanges.

Want to see which strategies apply to your rental portfolio? Run your free tax assessment — it analyzes your income, properties, and filing status against all 35+ strategies in under 2 minutes.

Related Reading

See How Much You're Overpaying

Run a free 2-minute assessment and get your personalized tax leak report — with IRS-backed strategies and IRC code citations.

Run My Free Assessment