Solo 401(k) vs SEP IRA: Which Retirement Plan Saves You More? (2025 Comparison)

Both let you shelter up to $69,000/year from taxes. But the Solo 401(k) wins for almost everyone. Here's the side-by-side math.

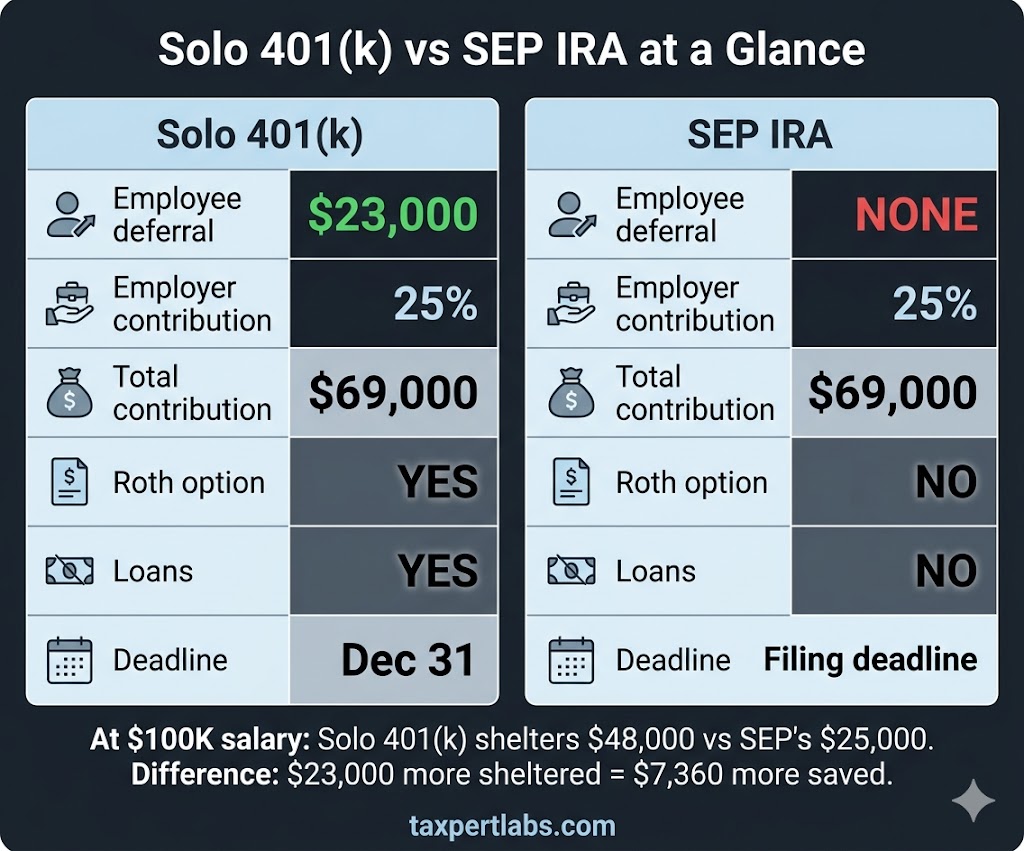

The Solo 401(k) and SEP IRA are the two most popular retirement plans for self-employed individuals. Both allow up to $69,000 in annual contributions ($76,500 if age 50+), both provide immediate tax deductions, and both offer tax-deferred growth. However, the Solo 401(k) is the better choice for nearly every self-employed professional because it allows an additional $23,000 in employee deferrals that the SEP IRA does not. This single difference can mean $7,000-$8,500 more in annual tax savings.

Side-by-side comparison: Solo 401(k) vs SEP IRA

| Feature | Solo 401(k) | SEP IRA |

|---|---|---|

| Employee deferral (2025) | $23,000 ($30,500 if 50+) | None |

| Employer contribution | 25% of W-2 (S-Corp) or 20% of net SE | 25% of W-2 or 20% of net SE |

| Total maximum (2025) | $69,000 ($76,500 if 50+) | $69,000 |

| Roth option | Yes | No |

| Loan provision | Yes (up to $50K or 50%) | No |

| Establishment deadline | December 31 of tax year | Tax filing deadline (with extensions) |

| Funding deadline | Tax filing deadline | Tax filing deadline |

| Employees allowed? | Owner + spouse only | Must cover all eligible employees |

| Admin complexity | Moderate (Form 5500 if over $250K) | Simple (no annual filing) |

The contribution math: why Solo 401(k) wins below $275K

At lower and mid-range incomes, the Solo 401(k) allows significantly higher total contributions because of the $23,000 employee deferral:

| S-Corp Salary | Solo 401(k) Total | SEP IRA Total | Difference |

|---|---|---|---|

| $60,000 | $38,000 ($23K + $15K) | $15,000 | +$23,000 |

| $100,000 | $48,000 ($23K + $25K) | $25,000 | +$23,000 |

| $150,000 | $60,500 ($23K + $37.5K) | $37,500 | +$23,000 |

| $200,000 | $69,000 ($23K + $50K, capped) | $50,000 | +$19,000 |

| $276,000+ | $69,000 (capped) | $69,000 (capped) | $0 |

At $100,000 salary, the Solo 401(k) shelters $23,000 more than the SEP IRA. At a 32% bracket, that is $7,360 in additional tax savings per year.

When the SEP IRA is the right choice

The SEP IRA wins in exactly two scenarios: (1) You missed the December 31 deadline to establish a Solo 401(k) — a SEP IRA can be opened and funded up to October 15 with an extension. (2) You have W-2 employees — SEP IRAs must cover all eligible employees at the same contribution percentage, but the admin is simpler than a full 401(k) plan.

For a detailed analysis of how retirement contributions interact with your full tax picture, run your free tax assessment. See also our S-Corp Savings Calculator to model the salary + contribution optimization.

Related Reading

See How Much You're Overpaying

Run a free 2-minute assessment and get your personalized tax leak report — with IRS-backed strategies and IRC code citations.

Run My Free Assessment