CPA vs Tax Strategist: Why Your Accountant Isn't Saving You Money

Your CPA files your return. A tax strategist finds the $30K-$100K your CPA isn't looking for. Here's the difference — and why you need both.

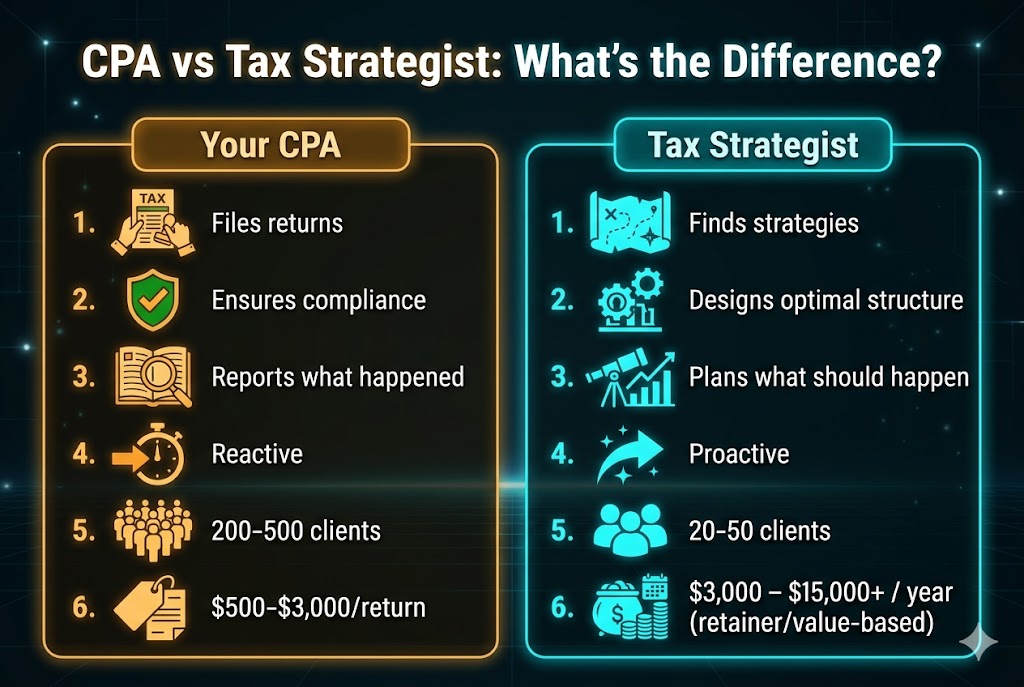

A CPA files your tax return. A tax strategist finds the strategies your CPA isn't looking for. These are fundamentally different jobs, and confusing them costs high-income professionals $30,000 to $100,000+ per year in unnecessary taxes. Your CPA is not failing you — they are doing exactly what they were trained to do. The problem is that what they were trained to do is compliance, not optimization.

What Your CPA Does

- Files your federal and state tax returns accurately

- Ensures compliance with IRS rules and deadlines

- Calculates your tax liability based on what happened

- Handles audits and correspondence with the IRS

- Prepares financial statements and bookkeeping

This is valuable work. You need it done correctly. But it is fundamentally backward-looking — your CPA reports what already happened.

What a Tax Strategist Does

- Analyzes your income against 35+ IRS strategies before year-end

- Designs optimal entity structure (LLC, S-Corp, C-Corp, or combination)

- Models scenarios — "what happens to your tax bill if you buy this property / make this election / contribute this amount"

- Identifies strategies your CPA hasn't suggested (S-Corp election, cost segregation, defined benefit plans, Augusta Rule)

- Creates implementation plans your CPA can execute

This is fundamentally forward-looking. A strategist designs what should happen. A CPA reports what did happen.

Why the Gap Exists

| Factor | CPA | Tax Strategist |

|---|---|---|

| Training focus | Compliance and accuracy | Optimization and planning |

| Timing | After year-end | Before year-end |

| Client volume | 200-500+ clients | 20-50 clients |

| Revenue model | Per-return fees ($500-$3,000) | Strategy fees ($5,000-$50,000) |

| Risk tolerance | Conservative (minimize audit risk) | Aggressive but defensible |

| Proactive outreach | Rare outside tax season | Quarterly or ongoing |

Your CPA handles 300 clients during a 3-month tax season. They do not have time to research whether you should elect S-Corp status, set up a Solo 401(k), do a cost segregation study on your rental, or implement an Augusta Rule strategy. That is not a criticism — it is a math problem. Strategy requires time they don't have.

What This Costs You

A Florida professional earning $300,000 with a standard CPA filing and no proactive strategy typically pays approximately $85,000 in federal taxes. With a proper tax strategy (S-Corp, Solo 401(k), business deductions, HSA, home office, vehicle), that same person pays approximately $35,000-$45,000.

The difference: $40,000-$50,000 per year — not because the CPA made errors, but because strategies that could have been implemented were never suggested.

The Solution: Use Both

The optimal setup for any high-income professional:

- Tax strategist designs the plan (entity structure, retirement, deductions, elections)

- CPA executes the plan (files returns, runs payroll, handles compliance)

- Strategist reviews CPA's work to ensure all strategies are properly implemented

Your CPA will thank you. They would rather implement a clear strategy plan than guess at what you might qualify for.

Want to see what your CPA is missing? Run your free tax assessment — we check your income against 35+ IRS strategies and show you every dollar you could be keeping. Takes 2 minutes. Hand the results to your CPA.

Related Reading

See How Much You're Overpaying

Run a free 2-minute assessment and get your personalized tax leak report — with IRS-backed strategies and IRC code citations.

Run My Free Assessment